uae-corporatetaxderegistration.com

Corporate Tax De-Registration in JAFZA Free Zone – Complete Guide

Complete guide to Corporate Tax de-registration in JAFZA Free Zone. Learn eligibility, FTA process, required documents, timelines, and compliance rules.

Gupta Group International

12/29/20253 min read

Corporate Tax De-Registration in JAFZA Free Zone – Complete Guide

Corporate Tax De-Registration in JAFZA Free Zone –Complete Guide

The introduction of UAE Corporate Tax has brought significant compliance obligations for businesses operating across the UAE, including those in the Jebel Ali Free Zone Authority (JAFZA). While JAFZA companies benefit from a robust free zone framework and potential 0% Corporate Tax under qualifying conditions, Corporate Tax registration and de-registration remain mandatory legal requirements.

This guide explains when Corporate Tax de-registration is required in JAFZA, the eligibility criteria, the de-registration process, timelines, penalties, and key compliance considerations for JAFZA Free Zone companies.

Understanding Corporate Tax De-Registration in JAFZA

Corporate Tax de-registration refers to the formal removal of a company from the UAE Corporate Tax register maintained by the Federal Tax Authority (FTA) through the EmaraTax portal.

A JAFZA company remains liable for Corporate Tax compliance until the FTA officially approves de-registration, regardless of:

Business inactivity

License expiry

Free zone status

Failure to de-register on time may result in administrative penalties, even if the company is no longer operational.

Corporate Tax Applicability for JAFZA Companies

Under Federal Decree-Law No. 47 of 2022, JAFZA entities are considered taxable persons once registered for Corporate Tax.

While many JAFZA companies may qualify as Qualifying Free Zone Persons (QFZP) and benefit from a 0% Corporate Tax rate, this does not eliminate compliance obligations, including:

Registration

Return filing

De-registration when applicable

Who Can Apply for Corporate Tax De-Registration in JAFZA?

A JAFZA Free Zone company may apply for Corporate Tax de-registration if:

The company has ceased all business activities in the UAE

The entity has been liquidated or struck off by JAFZA

The JAFZA license has been cancelled and the business is permanently closed

The business is no longer required to be registered under UAE Corporate Tax law

A dormant JAFZA company with no income is being formally closed

Important Note:

Even JAFZA companies enjoying QFZP status must apply for Corporate Tax de-registration if the business is closed or liquidated.

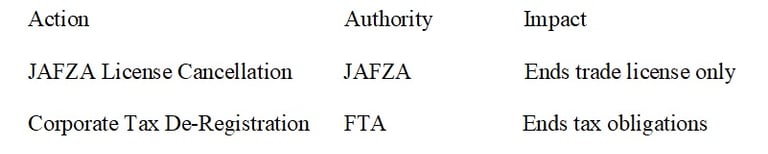

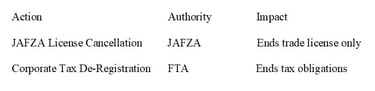

Corporate Tax De-Registration vs JAFZA License Cancellation

One of the most common misconceptions is that JAFZA license cancellation automatically cancels Corporate Tax registration. This is incorrect.

If Corporate Tax de-registration is not completed separately:

Filing obligations continue

FTA penalties may apply

Compliance notices may be issued

Key Conditions Before Applying for De-Registration

Before submitting a Corporate Tax de-registration application, JAFZA companies must ensure:

All Corporate Tax returns up to the cessation date are filed

Any outstanding Corporate Tax liabilities or penalties are settled

Final financial statements are completed up to the closure date

JAFZA license cancellation or liquidation is initiated or completed

The FTA may reject or delay applications if compliance requirements are incomplete.

Corporate Tax De-Registration Process for JAFZA Companies

The de-registration process is completed via the FTA EmaraTax portal and generally involves the following steps:

Step 1: Confirm Business Cessation

Ensure that all commercial activities have permanently stopped and the cessation date is clearly defined.

Step 2: Prepare Required Documents

Commonly required documents include:

JAFZA license cancellation or liquidation certificate

Final financial statements

Proof of business cessation date

Step 3: Submit De-Registration Application

Submit the Corporate Tax de-registration request through EmaraTax along with all supporting documentation.

Step 4: FTA Review and Clarifications

The FTA may request additional information or corrections before approval.

Step 5: Approval and Tax Account Closure

Once approved, the Corporate Tax registration is officially cancelled.

Timeline for Corporate Tax De-Registration in JAFZA

JAFZA companies are generally required to apply for Corporate Tax de-registration within three months from:

Business cessation

License cancellation

Completion of liquidation

Late applications may result in administrative penalties, even if no Corporate Tax is payable.

Corporate Tax De-Registration During JAFZA Liquidation

During liquidation, JAFZA companies must:

File a final Corporate Tax return

Declare any taxable income or losses

Settle outstanding liabilities

Submit liquidation and financial documentation to the FTA

The FTA will only approve de-registration once it confirms full tax compliance.

Penalties for Late or Incorrect De-Registration

The FTA may impose penalties for:

Failure to apply for de-registration within the required timeframe

Failure to submit final Corporate Tax returns

Providing incorrect or incomplete information

Ignoring FTA notifications

Penalties apply even to zero-income or QFZP-status companies.

Common Mistakes JAFZA Companies Should Avoid

Assuming dormant companies do not require de-registration

Believing license cancellation completes tax closure

Missing final return filing deadlines

Using incorrect cessation dates

Submitting incomplete documents on EmaraTax

These errors often lead to delays, rejections, or fines.

Why Professional Support Is Important

Corporate Tax de-registration in JAFZA involves:

Regulatory coordination between JAFZA and FTA

Accurate financial and tax reporting

Strict timelines and documentation requirements

Professional assistance helps ensure:

Correct sequencing of closure steps

Faster FTA approval

Avoidance of penalties

Complete compliance closure

© 2026 uae-corporatetaxderegistration.com