uae-corporatetaxderegistration.com

Corporate Tax De-registration In DMCC Free Zone – Complete Guide

Corporate Tax De-registration in DMCC Free Zone – complete guide covering eligibility, audit requirements, documentation, timelines, and compliance.

Gupta Group Inernational

12/29/20254 min read

Corporate Tax De-registration In Dmcc Free Zone – Complete Guide

Corporate Tax De‑Registration in DMCC Free Zone – Complete Guide

The introduction of UAE Corporate Tax has brought new compliance responsibilities for businesses operating in free zones, including the Dubai Multi Commodities Centre (DMCC). While many companies are required to remain registered, there are specific situations where Corporate Tax de‑registration in DMCC Free Zone becomes mandatory or advisable. This guide explains when and how DMCC entities can de‑register, along with key compliance considerations.

Understanding Corporate Tax De‑Registration in DMCC

Corporate Tax de‑registration refers to the formal removal of a business from the UAE Corporate Tax register maintained by the Federal Tax Authority (FTA). For DMCC companies, de‑registration is required when the entity ceases business activities, liquidates, or no longer meets the conditions for Corporate Tax registration

Failing to apply for de‑registration on time can result in penalties, even if the company is no longer operational.

Key Conditions Before Applying for De‑Registration

Before submitting a Corporate Tax de‑registration application, DMCC entities must ensure:

All Corporate Tax returns up to the date of cessation are filed

Any outstanding Corporate Tax liabilities are fully settled

Financial statements are finalized up to the closure date

DMCC license cancellation or liquidation process is initiated or completed

The FTA may reject de‑registration requests if compliance requirements are incomplete.

Corporate Tax De‑Registration Process for DMCC Companies

The de‑registration process is completed through the FTA Emara Tax portal and typically involves the following steps:

Step 1: Confirm Business Cessation

Ensure that all commercial activities have stopped and supporting documents are available.

Step 2: Prepare Required Documents

Commonly required documents include:

DMCC license cancellation or liquidation certificate

Final financial statements

Proof of business cessation date

Step 3: Submit De-Registration Application

Log in to the EmaraTax portal, select Corporate Tax de-registration, and submit the application along with supporting documents.

Step 4: FTA Review and Approval

The FTA will review the application and may request additional information. Once approved, the Corporate Tax registration will be officially cancelled.

Timeline for Corporate Tax De-Registration

Under UAE Corporate Tax regulations, de-registration should generally be applied for within three months from the date of business cessation, liquidation, or license cancellation.

Late applications may result in administrative penalties, even if no tax is payable.

Common Mistakes to Avoid

Assuming dormant companies do not need de-registration

Closing the DMCC license without updating Corporate Tax status

Failing to file final Corporate Tax returns

Ignoring FTA deadlines and notifications.

Proper planning and professional assistance can help avoid unnecessary fines and delays.

Why Professional Support Matters

Corporate Tax de-registration in DMCC involves coordination between:

DMCC Free Zone Authority

Federal Tax Authority (FTA)

Financial and compliance documentation

Errors or omissions can lead to penalties, rejection of applications, or future compliance issues.

Legal Framework for Corporate Tax De-Registration in DMCC

Corporate Tax de-registration in the DMCC Free Zone is governed by UAE Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses, along with subsequent Cabinet and Ministerial Decisions issued by the Federal Tax Authority (FTA).

Under this law, any taxable person—including Free Zone entities—must formally de-register when they cease to exist or cease to carry on business. Free Zone status does not exempt a company from this obligation.

DMCC companies are considered taxable persons once registered, and they remain responsible for compliance until the FTA officially approves de-registration.

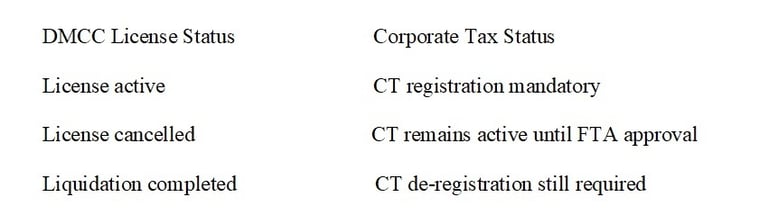

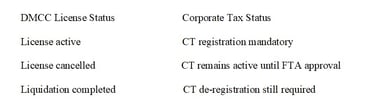

Corporate Tax De-Registration vs License Cancellation in DMCC

A common misconception is that DMCC license cancellation automatically cancels Corporate Tax registration. This is incorrect.

Failure to separately apply for Corporate Tax de-registration can lead to:

Continued filing obligations

Late filing penalties

System-generated fines from the FTA

Corporate Tax De-Registration for Dormant DMCC Companies

Many DMCC companies remain dormant for years with:

No revenue

No bank transactions

No operational activity

However, once registered for Corporate Tax, dormancy alone does not remove compliance obligations. A dormant company must either:

Continue filing nil Corporate Tax returns, or

Proceed with formal de-registration if the business is being closed

Ignoring the status may expose the company to penalties for non-filing, even if no tax is payable.

Corporate Tax Implications During Liquidation

During DMCC liquidation, companies must:

File a final Corporate Tax return covering the period up to cessation

Declare any taxable income or losses

Settle outstanding tax liabilities

Submit liquidation and financial documents to the FTA

The FTA will only approve de-registration once it confirms that all tax matters are fully resolved.

Penalties for Late or Incorrect De-Registration

The FTA may impose administrative penalties for:

Failure to apply for de-registration within the required timeframe

Failure to submit final Corporate Tax returns

Providing incomplete or incorrect documentation

Ignoring FTA requests or notices

Even zero-income or QFZP-status DMCC companies are not exempt from penalties if compliance steps are missed.

Documentation Checklist for DMCC Corporate Tax De-Registration

A complete and accurate document set significantly speeds up FTA approval:

DMCC license cancellation or liquidation certificate

Final financial statements (audited where applicable)

Proof of business cessation date

Final Corporate Tax return acknowledgment

Clearance of outstanding penalties or liabilities

Missing documents are one of the most common reasons for rejection.

EmaraTax Portal: Practical Considerations

While EmaraTax is the official FTA platform, DMCC companies often face challenges such as:

Incorrect cessation date selection

Mismatch between DMCC and FTA records

System validation errors

Requests for additional clarification

Professional handling helps avoid repeated submissions and delays.

Why DMCC Companies Choose Professional De-Registration Support

Corporate Tax de-registration is not just an administrative formality—it is a legal closure process. Professional assistance ensures:

Correct sequencing of license cancellation and tax closure

Accurate filing of final returns

Timely de-registration to avoid penalties

Complete compliance documentation

This is especially critical for shareholders planning to exit the UAE or close multiple entities.

© 2026 uae-corporatetaxderegistration.com